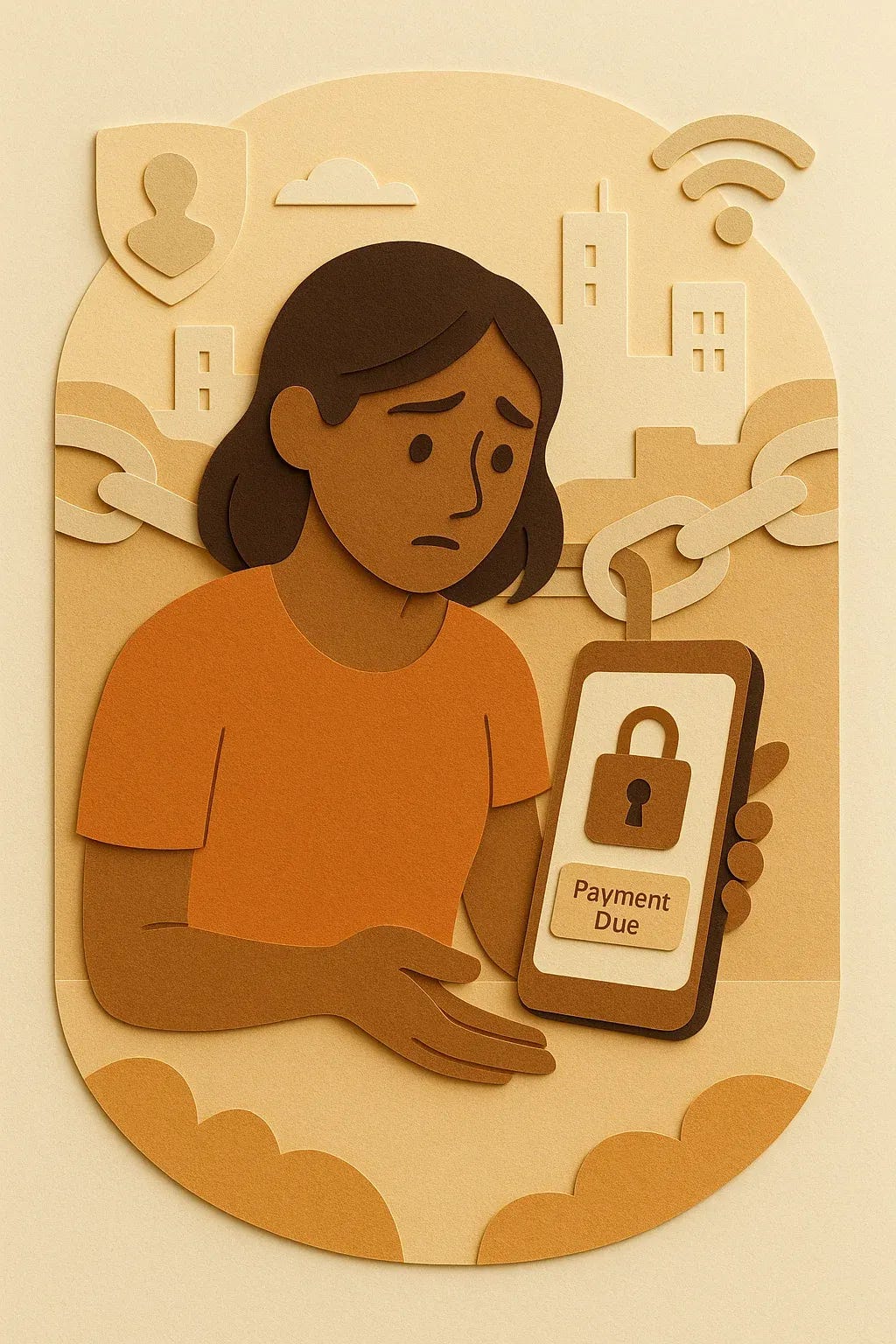

On a crowded street in Nairobi, a young shopkeeper pulls out her smartphone to pay a supplier. The screen flickers—and locks. A payment reminder flashes across the screen: “Complete your overdue installment to continue.” She sighs, juggling between keeping her business running and staying current on her phone loan.

This scene is not far-fetched—it’s already happening across Africa, Asia, and Latin America. Device locking has become the invisible gatekeeper of digital finance: ensuring repayment while sparking fierce debate about privacy, fairness, and consumer rights. As the technology matures, the question isn’t whether device lock will expand, but how it will be shaped—by AI, regulation, advocacy, and new user-centric design.

What follows is not a static snapshot, but a look forward. Trends today signal a future where device locking evolves far beyond smartphones, reshaping how lenders, telcos, and regulators think about enforcement and trust.

Trend 1:

AI as the New Arbiter of Credit and Privacy

Imagine a call center in Mumbai in 2027. Instead of human agents, AI models analyze repayment histories, flag risks, and trigger partial lockouts—while also explaining in plain language why the lock occurred.

This is the emerging face of device enforcement. Lenders are experimenting with AI to decide when, how, and to whom locks should apply. The promise is precision: fewer wrongful lockouts, better repayment rates, and more personalized credit terms. But the risks are equally vivid. Regulators in India, Europe, and soon LATAM are demanding AI transparency—algorithms must be explainable and auditable.

For telcos and fintechs, this means balancing innovation with compliance. Deploying AI without oversight could backfire, leading to lawsuits, loss of consumer trust, or outright bans. The winners will be those who bake privacy-by-design into their systems, showing not only that AI works, but that it respects users’ rights.

Trend 2: Regulation Tightens the Rules of the Game

Picture a future onboarding screen in São Paulo: before a phone is financed, the user swipes through visual simulations showing what a lock looks like, how to appeal it, and what services remain accessible.

Such transparency may soon be mandatory. Regulators worldwide are drafting tighter rules on consent, data localization, and consumer safeguards. In India and China, laws already dictate how user data can be stored.

In the EU, the AI Act will soon require full audit trails for any automated enforcement. In Africa and LATAM, policymakers are catching up—sometimes faster than the companies deploying these tools.

For lenders, this means device lock isn’t just a technical feature—it’s a compliance challenge. Approval of financing models may hinge on guarantees of emergency access, clear notifications, and limits on lock duration. The more consumer-friendly the safeguards, the smoother the regulatory path.

Trend 3: Advocacy Shapes the Moral Compass

In Kampala, a community radio station hosts a heated debate. NGO representatives argue that locking out a migrant worker from her only phone is not financial discipline—it’s digital exclusion.

This advocacy is no longer on the margins. Civil society groups are becoming a powerful counterweight to industry enthusiasm. Their campaigns push for emergency unlocks, multi-layered device security, and independent audits of locking software. In East Africa and beyond, their influence is visible in regulatory hearings and investor due diligence.

For the industry, ignoring this voice is risky. Investors and regulators alike are sensitive to reputational harm. Building transparent policies and dialogue with NGOs may soon be as essential as technical performance. Device lock providers that align with rights-based frameworks will have a stronger license to operate globally.

Trend 4: Beyond Phones—A Universal Enforcement Tool

Fast-forward to 2030. A solar home kit in rural Kenya dims its light at sunset—not because the battery is weak, but because the latest installment is overdue. In Mexico City, an e-scooter won’t start until the rider clears a missed micro-loan payment. In Jakarta, laptops for students come with built-in pay-as-you-go enforcement.

This is the trajectory already visible today. From Safaricom’s smartphone programs to M-Kopa’s solar kits, the lock/unlock model is spreading wherever credit meets essential hardware. What began as a lost-phone recovery tool has become the backbone of financial inclusion—if designed responsibly.

The implications are huge. Telcos, fintechs, and hardware makers are converging into new ecosystems of credit and enforcement. But with every expansion comes greater scrutiny: How do you guarantee that a locked scooter doesn’t endanger a commuter? How do you ensure a laptop lock doesn’t cut a student off from school? These questions will define the boundaries of the next wave of device enforcement.

Device locking is no longer just about securing repayment—it is becoming a test case for how technology, regulation, and human rights intersect in emerging markets.

The future will be shaped by tension: between AI precision and human oversight, between regulatory guardrails and market speed, between inclusion and exclusion. What’s clear is that privacy will be the axis around which innovation and trust must balance.

For lenders and telcos, the next decade is not just about deploying device locks—it’s about doing so in a way that wins user trust, passes regulatory muster, and supports financial inclusion. For regulators and advocates, it’s about ensuring that enforcement tools don’t deepen the digital divide.

The devices may change—from phones to scooters to laptops—but the core question remains: can we design enforcement that empowers rather than excludes?

How do you see device lock evolving in your market? Join the conversation in our ongoing: Device Lock & Privacy series